Convertible bond arbitrage is a strategy used mostly by hedge funds and professional investors.

The idea is to buy a convertible bond and at the same time short sell the companys stock. The investor tries to earn from the price difference between the bond and the stock while managing market risk.

It sounds technical at first, but the basic logic is simple.

A convertible bond has features of both debt and equity. It pays interest like a bond, but it can also be converted into shares of the company.

Because of this mixed nature, sometimes the bond may look cheap compared to the stock. Convertible bond arbitrage tries to take advantage of that situation.

What is a Convertible Bond?

A convertible bond is a bond issued by a company that gives the bondholder the option to convert the bond into a fixed number of shares.

For example, a company may issue a convertible bond with a face value of ₹1,000. The bond may be convertible into 20 shares.

This means the conversion price is:

₹1,000 / 20 = ₹50 per share

If the companys share price rises above ₹50, conversion becomes attractive.

If the share price stays below ₹50, the investor may continue to hold the bond and receive interest.

So, the investor has downside protection from the bond and upside potential from the equity conversion feature.

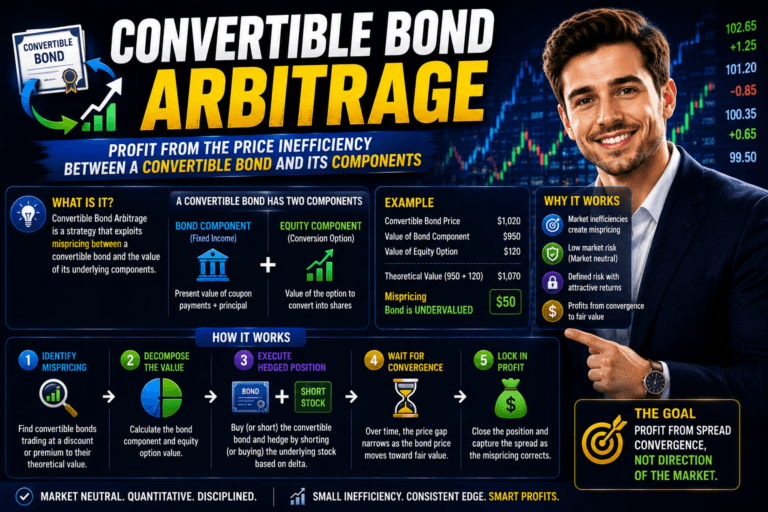

What Convertible Bond Arbitrage Means

Convertible bond arbitrage means buying the convertible bond and short selling the same companys stock.

The investor is not simply betting that the stock will go up or down.

Instead, the investor is trying to benefit from mispricing between the convertible bond and the underlying shares.

If the convertible bond is undervalued, the investor buys it.

To reduce equity risk, the investor shorts the stock.

This way, if the stock price moves, the gain on one side may partly offset the loss on the other side.

Simple Example

Suppose ABC Ltd has issued a convertible bond.

Bond price = ₹950

Face value = ₹1,000

Coupon = 5 percent

Conversion ratio = 20 shares

Current stock price = ₹45

The bond can be converted into 20 shares. So, the conversion value is:

20 × ₹45 = ₹900

The bond is trading at ₹950, which is slightly above its conversion value, but it also provides coupon income and bond protection.

Now suppose an investor believes the convertible bond is undervalued because the stock has strong upside potential and the bond still provides downside support.

The investor buys the convertible bond at ₹950.

At the same time, the investor short sells some shares of ABC Ltd to reduce the risk from stock price movement.

If the stock rises, the convertible bond becomes more valuable because the conversion option becomes more attractive. The short stock position may lose money, but the bond gain may offset it.

If the stock falls, the short stock position may make money. The convertible bond may lose some value, but it may not fall as much as the stock because it still has bond value.

This balance is the main idea behind convertible bond arbitrage.

Real Life Context

Assume a hedge fund is studying a technology company.

The company has issued convertible bonds, and its shares are actively traded.

The hedge fund believes that the market is undervaluing the convertible bond. The stock has become volatile, and that volatility makes the conversion option more valuable. But the bond price has not fully reflected this value.

So, the hedge fund buys the convertible bond.

To avoid taking a direct long position in the stock, it shorts the companys shares.

Now the fund is mainly trying to earn from the pricing gap between the bond and the stock, not from a simple bullish or bearish view.

If the stock becomes more volatile or the bond price moves closer to fair value, the hedge fund may benefit.

This is why convertible bond arbitrage is often used by funds that understand both fixed income and equity markets.

Why Investors Use This Strategy

Investors use convertible bond arbitrage because it can provide returns that are not fully dependent on overall market direction.

The strategy can earn from:

Mispricing between bond and stock

Coupon income from the bond

Changes in stock volatility

Credit spread movement

Conversion option value

Short stock hedge

The aim is not to take a plain equity bet. The aim is to manage risk and capture relative value.

Main Risks

Convertible bond arbitrage is not risk-free.

One major risk is credit risk. If the companys financial position weakens, the bond price may fall sharply.

Another risk is short squeeze risk. If the stock price rises very quickly, the short stock position can create losses.

There is also liquidity risk. Some convertible bonds are not traded actively, so exiting the position may be difficult.

Volatility risk is also important. If expected volatility falls, the value of the conversion option may decline.

The strategy also requires careful hedging. If the hedge ratio is wrong, the investor may remain exposed to unwanted stock price movements.

Why It is Called Arbitrage

In theory, arbitrage means earning profit from price differences with little or no risk.

But in real markets, convertible bond arbitrage is not risk-free arbitrage.

It is better understood as a relative value strategy.

The investor tries to find situations where the convertible bond is cheap or expensive compared to the stock and other market factors.

So, the word arbitrage is used because the strategy looks for mispricing, but there are still risks involved.

Final Thoughts

Convertible bond arbitrage is a strategy where an investor buys a convertible bond and short sells the underlying stock.

The goal is to benefit from mispricing between the bond and the shares while reducing direct equity risk.

It is mainly used by hedge funds and professional investors because it requires knowledge of bonds, stocks, options, credit risk, and hedging.

The simple way to remember it is this:

Convertible bond arbitrage tries to profit from the relationship between a convertible bond and the companys stock, instead of betting only on the stock moving up or down.