1) INTRODUCTION

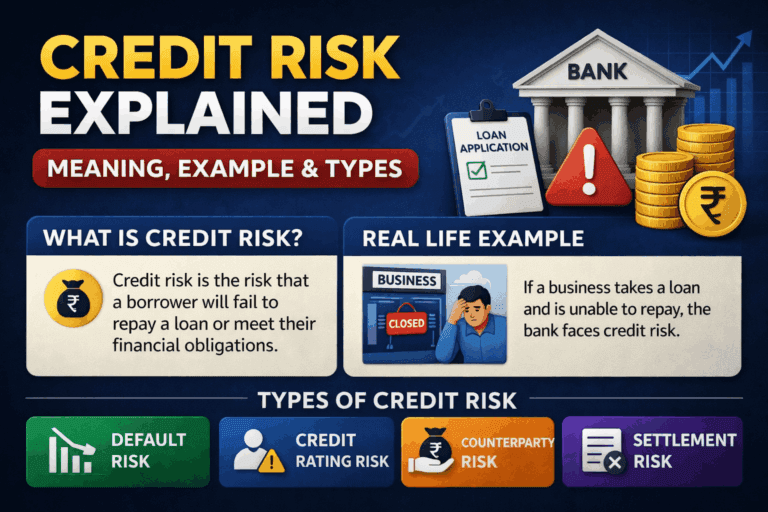

Credit risk is the possibility that a borrower will fail to repay a loan or meet their financial obligations. In simple terms, it is the risk that money lent may not be fully returned.

This concept exists because lending is a core activity in finance. Banks, financial institutions, companies, and even individuals regularly lend money through loans, bonds, credit cards, and trade credit. Since borrowers may face financial difficulties or default entirely, lenders must understand and manage credit risk to protect their capital.

Credit risk management helps financial institutions decide who to lend to, how much to lend, and what interest rate to charge.

2) KEY TAKEAWAYS

- Credit risk is the risk that a borrower cannot repay borrowed money.

- It arises in loans, bonds, credit cards, and trade credit between businesses.

- Financial institutions assess credit risk using tools like credit scores, financial analysis, and collateral.

- Higher credit risk often leads to higher interest rates or stricter lending conditions.

- Managing credit risk is essential for bank stability and financial system health.

3) CORE EXPLANATION

Definition

Credit risk refers to the possibility that a borrower will fail to meet debt obligations according to agreed terms. This failure is called default.

If default occurs, the lender may experience:

- Partial loss of money

- Delayed payments

- Legal recovery costs

- Complete loss of the loan amount

Credit risk exists in many financial products such as:

- Bank loans

- Corporate bonds

- Credit cards

- Mortgages

- Trade credit between businesses

Financial institutions use risk assessment methods to estimate the likelihood of default before lending money.

How Credit Risk Works

When a lender evaluates a borrower, they try to answer three key questions:

- Will the borrower repay the loan?

- What is the probability of default?

- How much could be lost if default happens?

To answer these questions, lenders examine several factors:

1. Creditworthiness

Borrowers are evaluated based on:

- Income stability

- Debt levels

- repayment history

- financial statements (for companies)

Individuals often have credit scores, while companies are assessed using financial ratios and credit ratings.

2. Interest Rate Adjustment

Higher-risk borrowers usually face higher interest rates. This compensates lenders for taking additional risk.

3. Collateral

Some loans require assets as security. If the borrower fails to repay, the lender can seize the collateral.

Examples include:

- Mortgages (house as collateral)

- Auto loans (vehicle as collateral)

4. Monitoring

Even after lending, financial institutions continuously monitor borrowers to detect signs of financial distress.

Types of Credit Risk

Default Risk

The risk that a borrower fails to repay the loan entirely or misses scheduled payments.

Counterparty Risk

Occurs when one party in a financial contract (such as derivatives or trading agreements) fails to meet obligations.

Concentration Risk

This arises when a lender has too much exposure to a single borrower, sector, or region. If that sector performs poorly, many loans may default simultaneously.

Sovereign Risk

The risk that a government may default on its debt obligations, affecting bondholders and lenders.

4) NUMERICAL OR REAL-WORLD EXAMPLE

Imagine a bank lending money to two individuals.

Borrower A

- Loan amount: $10,000

- Stable job and strong credit history

Borrower B

- Loan amount: $10,000

- Irregular income and previous missed payments

The bank estimates:

- Borrower A default probability: 2%

- Borrower B default probability: 12%

To compensate for higher risk, the bank may:

- Offer Borrower A a lower interest rate

- Charge Borrower B a higher interest rate

If Borrower B defaults and cannot repay the loan, the bank may recover only part of the amount through legal action or collateral. The unrecovered portion becomes a credit loss.

This example shows how lenders adjust decisions based on credit risk levels.

5) WHY THIS MATTERS

Credit risk plays an important role across the financial system.

For Banks

Banks lend large amounts of money. Poor credit risk management can lead to large losses and financial instability.

For Companies

Companies extend trade credit to customers. Evaluating credit risk helps avoid unpaid invoices.

For Investors

Investors buying corporate or government bonds must assess whether the issuer can repay the debt.

For Careers in Finance

Credit risk is a key field in:

- Banking

- Risk management

- Credit analysis

- Financial regulation

- Investment management

Professionals working in credit risk analyze borrower data, assess financial health, and build risk models.

6) COMMON MISCONCEPTIONS

1. Credit Risk Only Exists in Banks

Credit risk occurs in many places, including corporate lending, bond investing, and supplier credit agreements.

2. High Interest Rates Always Mean High Profit

Higher rates compensate for risk, but if default occurs, the lender may still lose money.

3. Collateral Eliminates Credit Risk

Collateral reduces potential loss but does not remove the risk completely. Asset values may fall or recovery may be difficult.

4. Credit Scores Tell the Full Story

Credit scores are useful indicators but lenders also evaluate income stability, debt levels, and financial statements.

5. Only Small Borrowers Default

Large corporations and even governments can default on debt obligations.